Liquidity risk

Challenges

Fast and simple calculation of regulatory liquidity reports

Continuously increasing regulatory requirements and a high market volatility together with high income expectations require banks to apply an active and professional risk management. This includes an active management of the liquidity risk relevant to banks .

Solutions

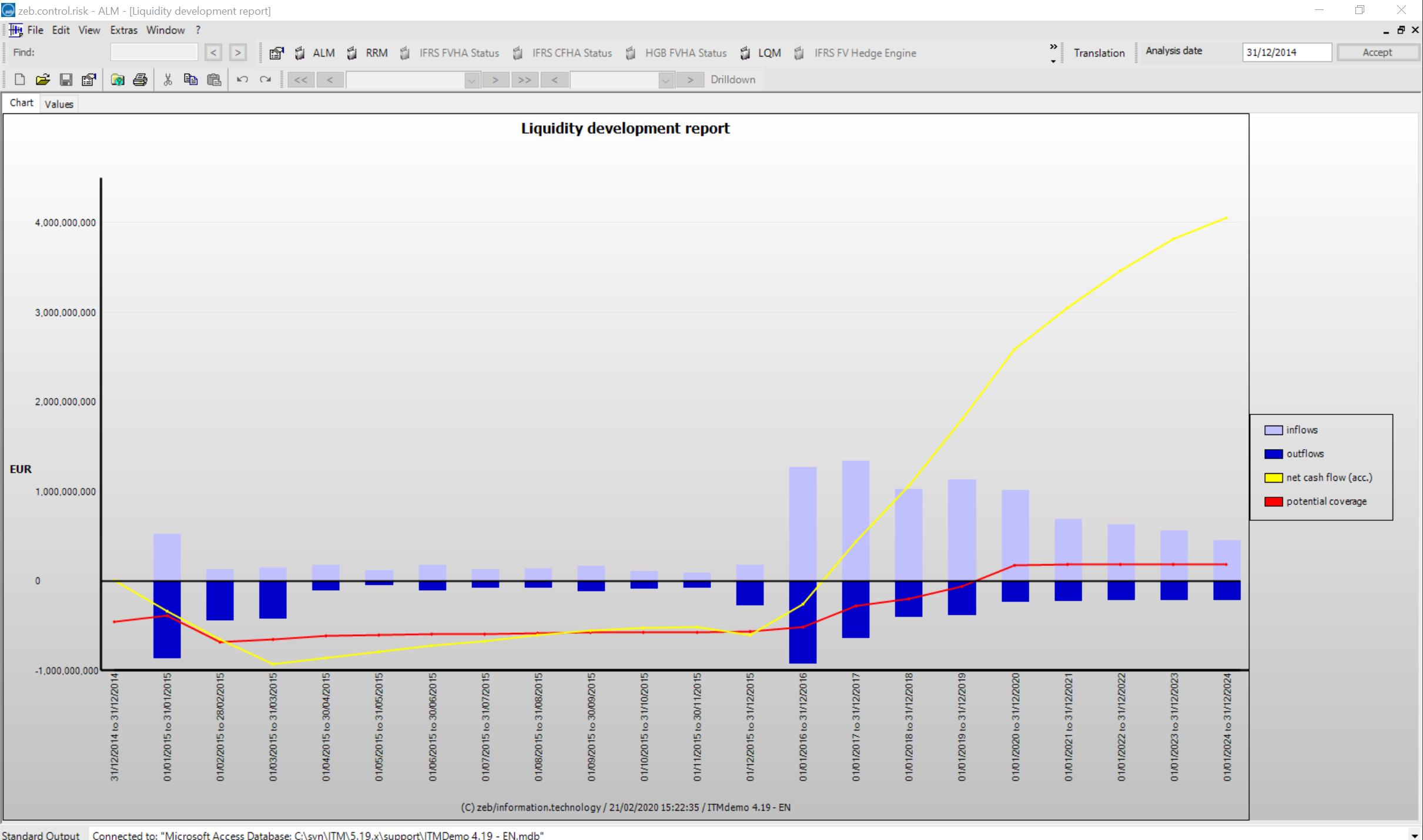

The Liquidity Manager module fully covers the required risk management process

- Generation of liquidity cash flows for individual transactions

- Aggregation according to freely selectable criteria on the basis of a portfolio model to provide liquidity overviews

- Implementation of stress testing using the parameterized risk characteristics

- Derivation of a survival horizon of the bank in a crisis situation (insolvency risk)

- Calculation of the minimum liquidity buffer and indirect costs

- Calculation of the present value-based funding loss (structural liquidity risk)

Benefits

- zeb’s expert knowledge of risk management topics as well as of legal and regulatory requirements

- Security through proven solutions and compliance with regulatory requirements

- Transparency about the risk situation with regard to liquidity

- Sustainability through continuous development with regard to professionalism and usability

References

Excerpt of our customers

Contact

Your contact persons

David Benz

Malte Jacobsen