zeb.control »

Impairment

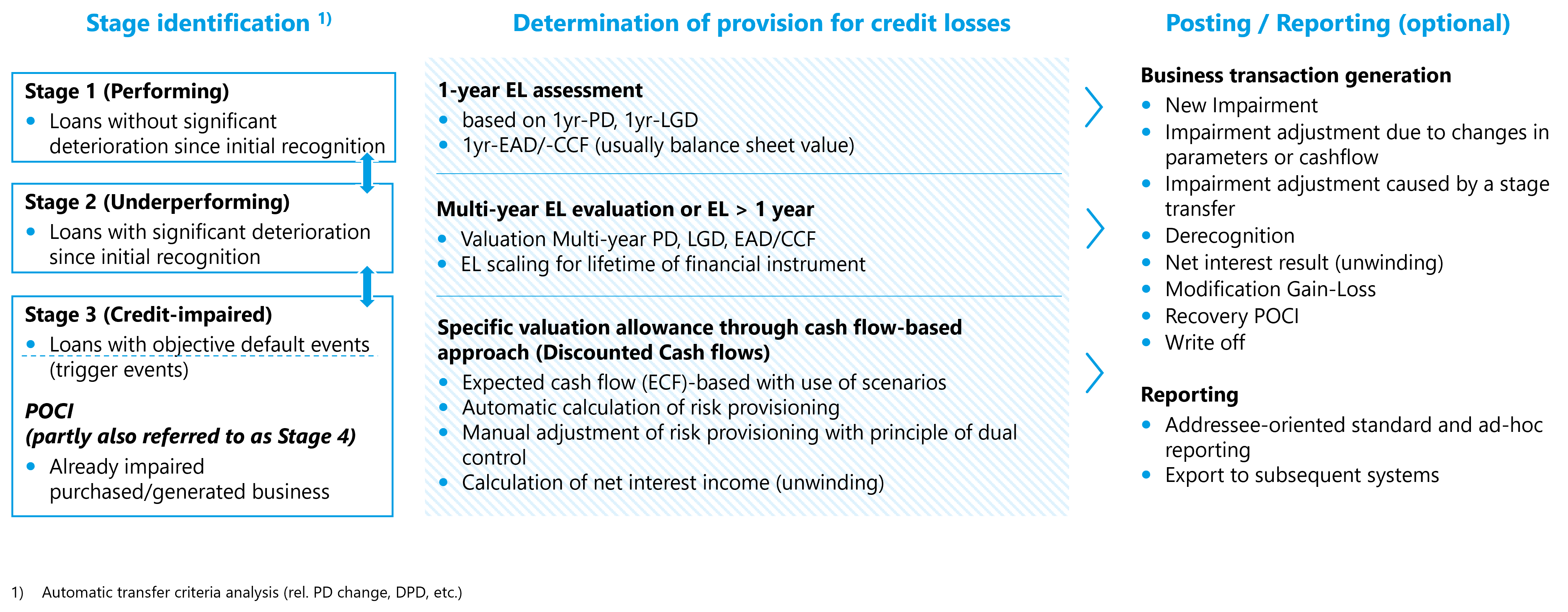

IFRS 9-compliant implementation of the impairment process from data delivery to posting.

Challenges

Compliance with the regulatory and commercial law provisions for Impairment

Unforeseeable impairments are not uncommon. It is essential to determine that they comply with IFRS for accounting purposes. An early implementation of the EL-based impairment model, test calculation for the management of the future P&L volatility and creating transparency for the transition pose particular challenges. In addition, reviewing and tracking periodic credit quality changes for (re)allocation to the three-step logic should be accelerated.

Solutions

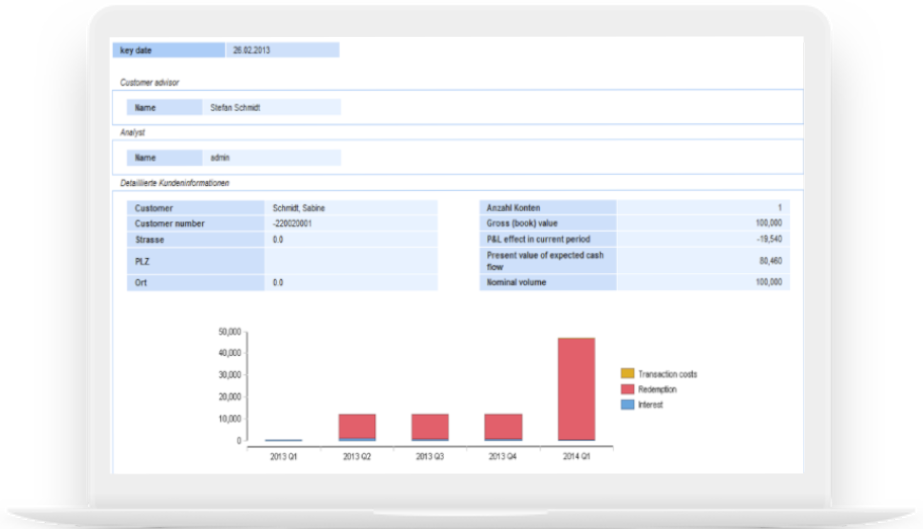

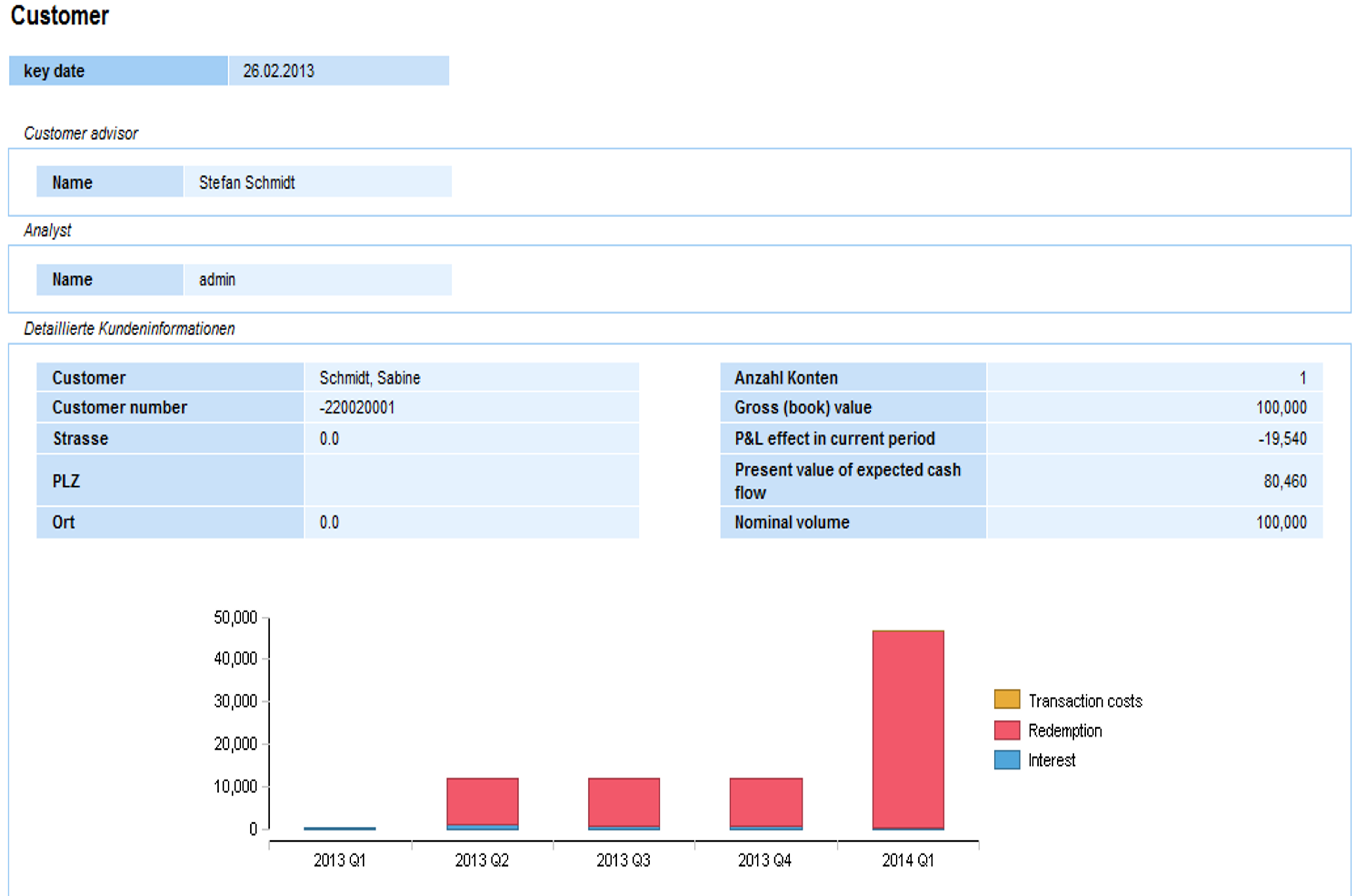

Complete representation of the entire IFRS process with zeb.control

- Implementation of the multi-level impairment process from data delivery to posting

- Calculation of specific and general loan loss provisions and unwinding effects in accordance with IFRS

- Institution-specific definition of step transfer criteria depending on borrower groups, volume, etc.

- Development of suitable EL/ELL calculation models and analysis of quantitative effects

- Clearly arranged representation of the status of the different periods with a directly visible P&L impact

Benefits

- Fully compliant with IFRS 9

- Parallel representation of IFRS 9 as well as HGB and UGB regulations

- Includes all, even complex valuation models

- Maximum flexibility in the delivery of parameters

References

Excerpt of our customers

Contact

Your contact persons

Detlev Ahrens

Lars Aupers

Ulrike Doering