Interest Rate Risk Management

The new generation of digital bank management platforms in treasury.

Increasing regulatory requirements and market volatility

Banks face the challenge of aligning high earnings expectations with a professional analysis of potential future developments to meet increasing regulatory requirements and market volatility. At the same time, a future-proof software solution requires the rapid implementation of technical requirements while considering current IT standards and a user-friendly interface. Additionally, financial institutions must harmonize control impulses from present value and periodic planning to manage the balance sheet structure effectively and control bank-wide interest rate and liquidity risks.

Agile treasury management through comprehensive interest rate risk management

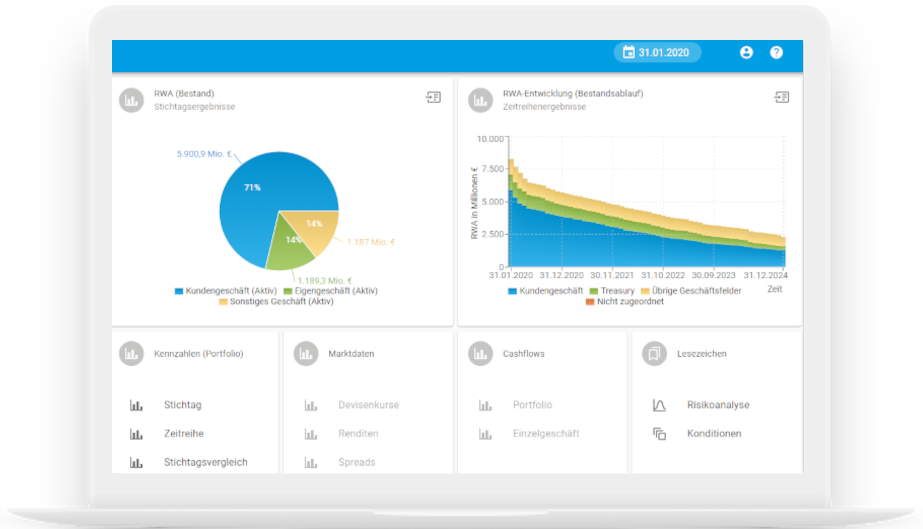

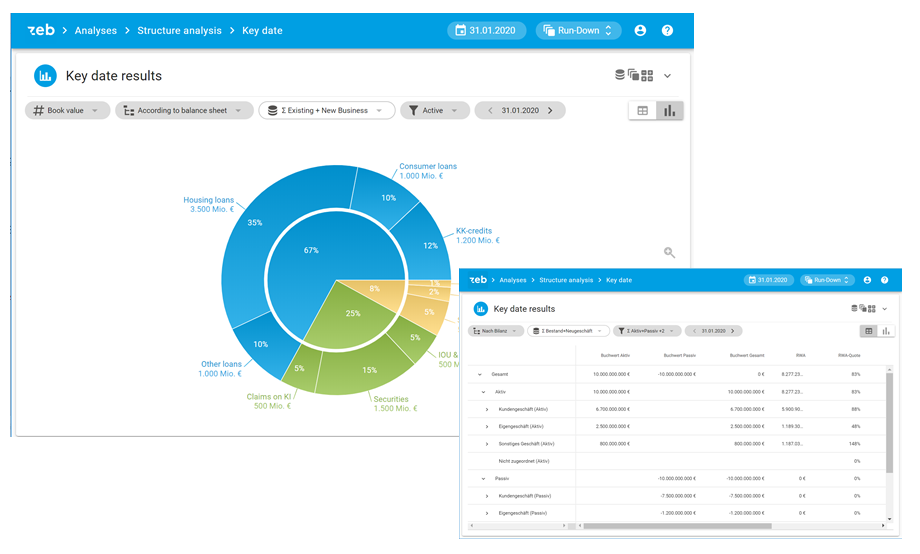

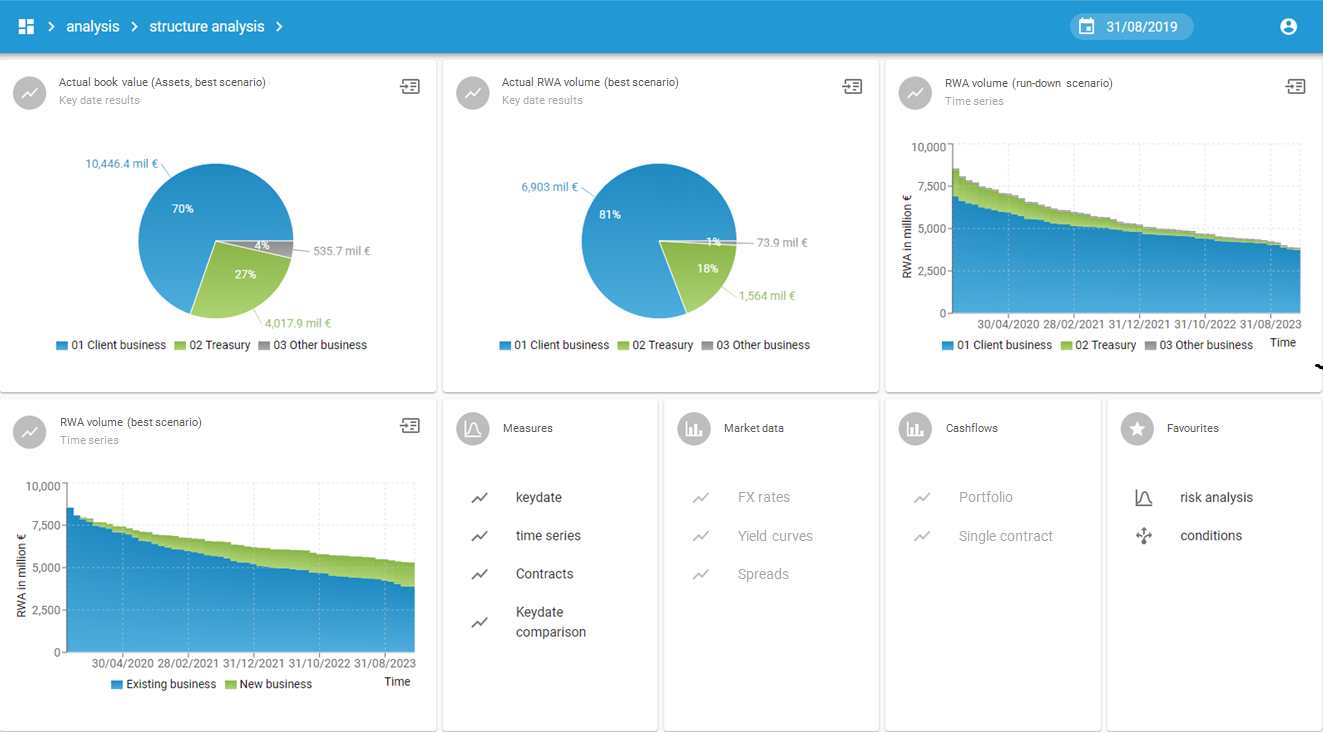

The Interest Rate Risk Management module provides comprehensive support for bank management through powerful simulation capabilities that allow for a detailed analysis of various market developments and hedging measures. This includes the simulation of the balance sheet and profit and loss statement on both a periodic and present value basis, the modeling of standard interest rate shocks, and the definition of customized market scenarios. An integrated scenario management system enables the clear administration of different scenario types and allows both manual and automated derivation of measures.

The digital advancement of bank management with zeb.control combines proven professional excellence with modern, future-proof service offerings. A high-performance architecture enables parallelized calculations of complex scenarios while also increasing computational performance, thereby unlocking new analytical capabilities. The platform meets current IT standards, including access via mobile devices and various operating models such as Software-as-a-Service and Pay-as-you-go. The user interface has been further developed to ensure an intuitive, results-oriented structure. By incorporating familiar web design concepts and enhanced reporting functionalities with comparative reports and graphical evaluations, user-friendliness is improved, supporting an exploratory and flexible working approach.

Additionally, the Interest Rate Risk Management module serves as a proven tool for asset and refinancing management. It provides extensive results planning and control, acting as a key instrument for overall bank management. Essential functions include a detailed compilation of the bank-wide cash flow, the simulation of annual financial statements, and the forecast of equity development while considering various planning parameters and scenarios. Furthermore, the system enables precise predictions of net interest income and valuation results, as well as the creation of a detailed interest income statement, taking into account margin and structural contributions. With this, zeb.control offers a comprehensive, future-proof solution for optimizing management processes in banks.

Greater transparency and targeted optimization of interest income

• Early identification of required actions through precise simulations

• Transparent representation of potential future developments in interest income

• Targeted utilization of optimization potential for improved results

Efficiency and cost advantages through modern technology

• Time savings: Simulations with short processing times of just a few minutes

• Lower operating costs: Software-as-a-Service model reduces ongoing expenses

• Efficient work processes: Optimal software support for exploratory analyses

Professional excellence and regulatory compliance

• More than 30 years of zeb expertise in asset-liability management

• Treasury know-how from zeb directly integrated into the solution

• Transparency over the structure of the interest rate book for sound management

• Compliance with regulatory requirements for secure bank management

Excerpt of our customers

Your contact persons

Articles you might be interested in